An entrepreneur’s income drives everything. Income drives the firm, personal goals, and should be a major factor when investing financial capital. By understanding your business cycle, risk tolerance, and personal goals a well thought out investment management strategy can lead to greater long-term results.

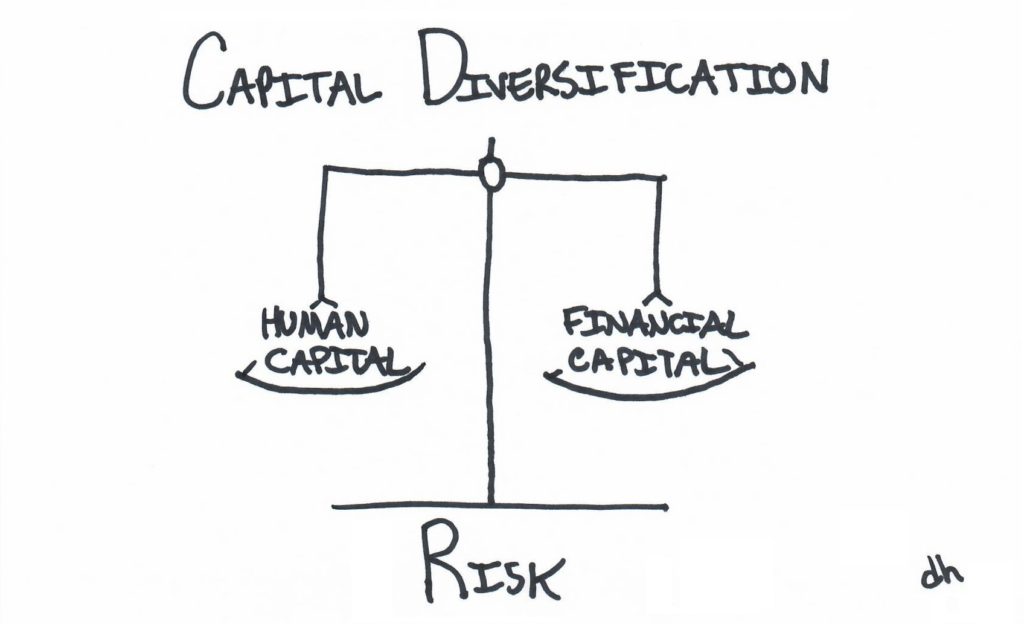

The Distinction between Human v. Financial Capital.

Human capital represents an individual’s ability to earn and save over time. The economic value for the entrepreneur fluctuates based on the successes and failures of the firm, much like a stock price rises and falls on the successes and failures of a publicly traded company. As a firm owner, human capital can be measured by the economic value of firm – perpetuated over its lifetime.

Financial capital represents saved resources typically measured in dollar value. Here, people and companies have control over how they would like to put this capital to work: many entrepreneurs reinvest into the businesses they are building, capital can be saved for future consumption (i.e. retirement income), and is consumed to support lifestyle today. Each dollar has its own expected return depending on where the dollar is invested and how it is managed over time.

Capital Considerations: Firm Owner v. Salaried Employee

It is important for a firm owner to understand the difference between their own human capital and a salaried employee’s as it has a difference when developing investment management strategies. Unless the salaried employee is 10 to 12 years away from using their financial capital (e.g. retirement income) they have the capacity to take a fairly large amount of financial risk, perhaps investing a majority of their financial capital in the stock market and other risky assets. Much of the reasoning behind this is based around their income – receiving a paycheck twice a month is like collecting interest on a bond, it is relatively stable and keeps on coming. Looking at the bigger picture, the salaried employee has a diversified portfolio, their human capital is invested in what is tantamount to bonds, while their financial capital is invested in stocks.

The entrepreneur, however, rides (perhaps drives) a different train. A firm owner’s income (human capital) may not be as steady as the employee and acts much like a stock: high risk, high reward and based off the success and failures of the firm. Investing all of your financial capital into risky assets like stocks then concentrates human and financial capital into the high-risk category when looking at the bigger picture. To create a more diversified portfolio is may be prudent to allocate a portion of financial capital to risk-hedging assets that zig when your growth assets (business and other investments) zag. By implementing this strategy the firm owner has an increased likelihood of fighting through tough times, maintaining personal goals, and being prepared for the pending recovery.

Investment Management Considerations for the Entrepreneur

Now I am not saying a firm owner should invest all their financial capital into risk-hedging assets. Heck, we are entrepreneurs, we like taking risk, and sure as **** love the returns that potentially come with it! I more advocate for proper planning and implementation. Take a look at your business and project what revenue would look like if it fell by 15%, by 30%, by 45% for a period of two to three years? How much additional cash would you need to keep paying employees, rent, and overhead? How much additional cash would you need to keep paying the mortgage, lifestyle, and children’s tuition?

The amount you choose to allocate to risk-hedging assets depends and varies much on your firm and the amount of risk you are willing to take. On one hand, if you operate a defense litigation firm and have a long and trusted relationship with a company that is constantly litigated against then income may be fairly consistent and the allocation to risk-hedging assets may be relatively low. On the other hand, if your firm operates primarily off contingency fees then perhaps a larger portion of financial capital be allocated to risk-hedging assets. In fact, in this particular area of law the concepts discussed almost naturally arise due to the powerful ebbs and flows of the contingency revenue model.

Going through a planning exercise like the one above will give the firm owner an idea of how much financial capital to allocate to risk-hedging assets. When investing these assets the key themes are preservation and liquidity. Although not sexy, investment grade bonds have historically been a stable hedge against the general economy. Over the past two major market downturns investment grade bonds have vastly outperformed the stock market and served as a consistent hedge against the market for decades. Additionally, these assets should be held in a non-retirement account, you never quite know when you may need access to the funds.

To boil this down it goes back to understanding who you are, what type of business you are running, and how to best allocate your resources so you are prepared for today, building for tomorrow, and protected from what may lie ahead. Should you have any questions or want to dig deeper I recommend working with an industry-specific consultant and/or a skilled financial planner.

Drew Hefflefinger is a CERTIFIED FINANCIAL PLANNER™ at Engage in Wealth in Denver, Colorado. Drew specializes in working with legal professionals by helping them preserve and grow wealth while achieving life goals. Drew can be contacted at drew@engageinwealth.com.